BEVAN GRAHAM: NZ monetary policy – the cycle, structural challenges and the war

Salt Funds economist Bevan Graham dives into some of the issues facing the RBNZ.

Bevan Graham is an economist at Salt Funds Management.

At Salt, our view on New Zealand monetary policy has always been shaped by one consistent theme: in a low potential growth economy, it does not take much for policy to shift from broadly neutral to actively stimulatory or contractionary.

That makes both the level of interest rates, and the speed at which they are adjusted, particularly important.

Executing this well is critical in achieving one of the core rationales of price stability – smoothing the economic cycle.

We have previously been critical of the Reserve Bank of New Zealand for not always getting this right, being at various times to slow to ease and at others, too slow to tighten, exacerbating both the interest rate and economic cycle.

To that point, regular readers of our research will recall that we were somewhat dubious about the need for last year’s final 75 basis points of cuts in the official cash rate to 2.25%, well below our estimated neutral range of 3-to-3.5%.

Weak economy

While the economy was undoubtedly weak, there were already tentative signs of stabilisation at that time. More importantly, New Zealand’s combination of low productivity growth and persistent capacity constraints suggested that the neutral rate was higher than many had become accustomed to in the pre-pandemic era.

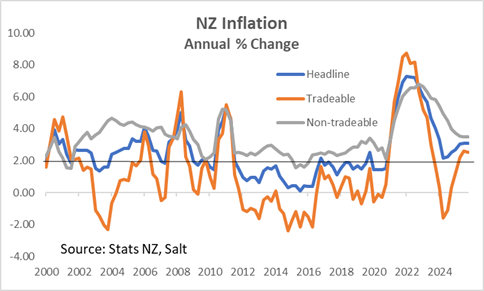

At the same time, non-tradable inflation remained sticky, a reminder that domestic cost pressures had not fully dissipated.

That backdrop led us to a relatively simple conclusion that if the OCR was pushed below neutral, it was unlikely to remain there for long. Some of that stimulus would, in time, need to be taken back, and perhaps quite quickly.

But equally important is how that adjustment occurs.

Our long-standing view has been that the earlier policy begins moving back toward neutral, the less likely it is that the RBNZ is forced into a sharper, more disruptive correction later.

Delay that adjustment, and the risk is that inflation proves more persistent, expectations become less well anchored, and the eventual response becomes more abrupt.

Recent March quarter CPI data reinforced that story.

At a time when the headline rate is moving higher due to the sharp increase in fuel prices and the focus is rightly on second round effects, non-tradable inflation remains firm, pointing to underlying domestic pressure that has yet to fully unwind.

Absent the uncertainty created by the war, that backdrop would argue for an earlier removal of monetary policy stimulus, consistent with our long-held view that policy set below neutral would need to be revisited sooner rather than later.

Subsequent developments have, in many respects, reinforced that thinking. The domestic economy has started to recover, while inflation has not retreated as much as hoped.

The familiar New Zealand dynamic remains – weak trend growth does not eliminate inflation pressure when supply capacity is equally constrained.

The war has complicated the story. Higher energy prices and renewed global uncertainty create a more difficult policy trade-off.

In the near term, the impulse is stagflationary with weaker growth alongside higher headline inflation. That muddies the signal for policymakers.

The governor of the RBNZ’s recent speech provides a useful lens here.

The emphasis has been on avoiding an overreaction to near-term inflation that monetary policy can do little to influence, while remaining alert to the risk that more persistent price shocks begin to feed into inflation expectations and broader wage- and price-setting behaviour.

In other words, the distinction between a temporary relative price shift and a more durable inflation process has become central to the reaction function.

Different to covid

At the same time, it is important to recognise that this cycle is not a repeat of the covid period. The RBNZ is understandably cautious about repeating the policy mistakes of that era.

But the starting point today is meaningfully different.

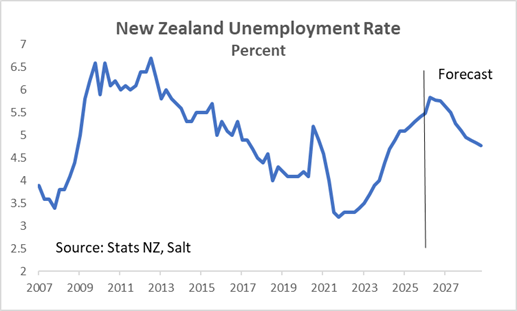

At the onset of covid, the economy was stronger and the unemployment rate was a tad over 4%. Today, the economy is softer, spare capacity is more evident, and the unemployment rate stands at 5.4%.

In fact, with the faster-than-expected recovery in net inward migration and the possibility of a war-related delay to firms implementing their hiring intentions, the unemployment rate could yet head higher.

That weaker starting point should act as a natural constraint on the degree to which higher fuel costs translate into broader, second-round inflation pressures.

In that sense, while the war complicates the near-term outlook, it may also reduce the risk of a sustained inflation overshoot relative to past episodes.

For now, that likely argues for a degree of patience, but it does not remove the underlying tension.

Because the longer policy remains away from neutral, even for understandable reasons, the greater the risk that the eventual adjustment becomes more abrupt.

And with domestic inflation pressures proving sticky, the case for beginning that adjustment is building.

At some point, the RBNZ is likely to need to begin withdrawing stimulus again, potentially sooner rather than later, even if the precise timing remains uncertain.

We expect to see interest rate increases before the end of the year with September most likely in our view.

That said, it’s not a view we would thump the table on.

A prolonged Iran conflict could see that first hike pushed out. Interest rate markets have recently been pricing around a 50% chance of a hike in the OCR as early as next month.

I think that’s way too soon, but the reality is the window for a smooth return to neutral will not stay open indefinitely, regardless of the outcome of the war.

Image from Curious News.

Disclosure: The Bottom Line editor Paul McBeth has owned units of Salt Funds Management’s long-short fund since January 2024. This commentary was provided free of charge by Salt's Bevan Graham.